This flexible product can give you access to the cash you need, when you need it.

A line of credit can be a valuable option for your business to bridge a cash flow shortfall. When used strategically, it can also be a powerful growth driver. Here’s what you need to know about lines of credit and how to use one to strengthen your business.

What is a business line of credit?

A business line of credit provides fast and flexible access to cash when and where you need it. Unlike a one-time lump sum loan, a line of credit can be used, paid down, and used again multiple

times. When you access funds through a line of credit, interest is only charged on the funds you use, and you can choose how much you want to access based on your business needs.

Lines of credit may be secured or unsecured:

- A secured line of credit requires collateral, such as real estate or another item of value, to guarantee repayment.

- An unsecured line of credit does not require such a guarantee.

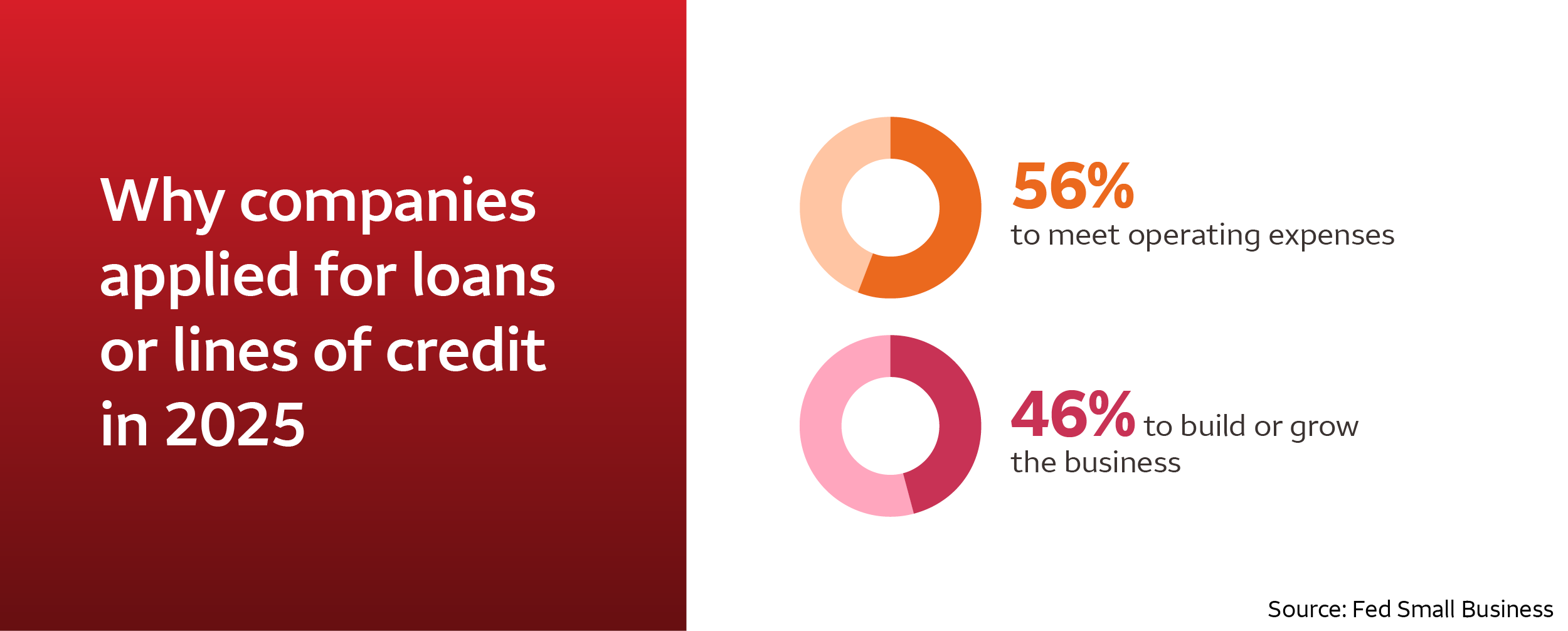

Source: Fed Small Business

How can your business use a line of credit?

There are several ways you can use a line of credit — for example to cover operating expenses or to invest in and expand your business.

1. Covering short-term cash shortages

Some businesses may have uneven cash flow. Whether you run a seasonal business that needs to bridge the gap for a few lean months or you’re waiting on a late invoice, a line of credit can offer a solution. Accessing cash through your line of credit can help you continue operating smoothly, keep your payment history intact and your vendor relationships in good standing.

2. Maximizing growth opportunities

When opportunity knocks, a line of credit can help you answer. Sometimes, a new client or expansion opportunity may require upfront spending, such as a large supply, expensive equipment or a software purchase. A line of credit can provide the cash needed to make those expenditures and help your business grow or operate more efficiently.

3. Hiring talent

The right people can make all the difference in how your business operates and grows. But, making an important new hire or adding new team members requires some upfront investment. A line of credit can help you meet the salary and benefit needs of the people who will take your business to the next level.

4. Building your business credit

Good business credit may unlock benefits like access to additional financing options, better interest rates, and more favorable terms with trade vendors. Managing a line of credit well and making timely payments can help build your business credit profile, potentially giving your company more financial options.

5. Giving you payment flexibility

A line of credit provides flexibility when paying for products and services. For example, your business may face a situation where using a business credit card isn’t possible because the interest rate is too high or the vendor doesn’t accept credit cards. A line of credit may be a better option in some situations because it may have a higher credit limit and can be used like cash, checks or electronic payments.

Exploring a line of credit for your business

A bank may require a business to have been operating for a minimum period of time, though exceptions exist, so be sure to check eligibility when considering product options. Wells Fargo offers line of credit options that are unsecured or secured, with limits ranging from $10,000 to $3,000,000, depending on the type of line.

As you weigh whether a line of credit is right for your business, be sure to consider:

- Total cost of the loan, including interest rates, which may vary, and fees like annual fee or fees for accessing the funds through an ATM or wire transfer

- Requirements like personal guarantees from or minimum credit scores for owners

Contact a Wells Fargo banker to learn more about lines of credit and to find out which line may be best for your business. To start using an existing line of credit, log in to your account.