There are a number of ways to fund your business.

Whether you’re starting, buying or growing a business, there are several ways to fund your goals. From traditional bank loans to online lenders and grants, business financing options can help support cash flow, manage risk and fuel growth.

So, what’s the best way to finance a business? That depends on your business goals, how much you need, and how quickly you need it.

What’s the best way to finance a business?

There’s no one “best” way. Different financing options suit different situations. The “right” kind of financing varies depending on the purpose, the amount your business needs, and whether you need short-, medium-, or long-term financing. It can also vary depending on how long you’ve had your business and your credit history. Here are a few options you might want to consider.

Bank loans

This is the most common form of business financing. Bank loans typically offer lower interest rates, predictable repayment terms, and the option to borrow larger amounts. There are different kinds of business financing, including term loans, lines of credit, and commercial real estate loans, which can be short- or long-term, depending on your specific needs.

Some loans are designed for short-term needs like equipment purchases or seasonal inventory. Others are for long-term investments like expansion or property acquisition. A banker can walk you through the options that fit your business needs.

When considering a business loan, you’ll want to calculate the monthly payment to see how it fits into your operating budget. Let’s say you have a $100,000 business loan with a five-year repayment period and 7% interest. That could result in a monthly payment of around $2,000. Actual terms can vary depending on your lender and credit profile.

Once you’ve settled on the type of loan, take time to prepare a strong application. Besides hard numbers like balance sheet and personal income, lenders also consider your business plan, your experience as a business owner and vision for growth. The more detailed and strategic your plan is, the more confident a lender can be about supporting your loan application.

SBA loans 2

SBA loans are issued by participating banks and financial institutions with a percentage of the loan guaranteed by the U.S. Small Business Administration. Because the government helps take on some of the risk to the lender, SBA loans may offer more flexible requirements and longer repayment terms than conventional bank loans. SBA loan amounts can vary from a few thousand dollars to up to $5.5 million.3 These loans can be used to buy equipment, real estate or fund long-term growth — or a combination of all uses (SBA 7(a)).

There are different options for SBA loans depending on your needs and eligibility. If you are eligible for SBA loans, they may make qualifying for credit more accessible and may provide an affordable option for your credit needs.

If you’re interested in applying for an SBA loan, talk to a banker who has experience in business credit, especially SBA lending, to ensure you understand all your options, as well as eligibility and collateral requirements and terms and conditions. From there, you can move on to the application process.

Can a new business get an SBA loan?

Yes, if you meet the eligibility requirements, SBA loans may be available to new businesses. Some common requirements include having a solid business plan, good personal credit and demonstrated ability to repay the loan.4

Seller financing

Sellers of big-ticket items like real estate, large equipment, or vehicles sometimes offer financing directly to the buyer. The financing may come with sales incentives, such as 0% interest for a specified period or lower sticker prices. Seller financing is highly flexible. The buyer and seller negotiate the terms: how much down payment, the interest rate, repayment schedule, closing costs, and other conditions.5 Because everything is through negotiation, not by bank or market standards, the interest rate can be higher or lower than what a bank might offer.

Factoring (accounts receivable financing)

This is a way to get the money from your business’s accounts receivable earlier by selling an invoice to a bank or a finance company in exchange for a percentage of the invoice amount. The factoring company will generally take a percentage or fee, resulting in your business receiving an amount lower than the face value of the invoice. This can be an option if your business is in need of immediate cash flow.

Online lenders and peer-to-peer loans

There are a growing number of online-only business lenders offering a variety of loan products. For companies with limited credit history, online lenders may be the easiest business loans to get. These loans tend to have more flexible criteria than traditional banks, but may come with higher interest rates or shorter terms. Be sure to compare offers and read the small print. While online lenders generally have higher approval rates than banks, they are less likely to provide the full amount of financial sought and have some of the lowest satisfaction rates, according to a yearly survey by the 12 Federal Reserve banks.6

Peer-to-peer (P2P) lending is online platforms that connect businesses with investors willing to buy or invest in the loan. Some specialize in short-term loans or lines of credit, which can help manage seasonal cash flow.

Personal financing

Many business owners turn to personal financing when just starting out. This might include personal credit cards, tapping into home equity, or applying for a personal loan. While this can be an effective way to launch a business, it puts your personal credit on the line. Lenders will consider both your business finances and personal credit history. If an application was turned down, it’s advisable to find out why to improve and apply again.

Community development grants or loans

There are nonprofits dedicated to helping businesses by providing loans and grants, usually backed by donations or government funds. Grants are funds awarded by government agencies or other organizations and don’t need to be repaid. They are typically designed to help specific types of businesses, such as those owned by veterans, women or operating in underserved communities.

Take the next step

Want to learn about financing options open to you and your business? Make an appointment to talk to a banker about your goals, your timeline, and how much funding you may need. A banker can help you:

- Explore loan and credit options that are based on your business size and stage.

- Understand what documents and qualifications you’ll need.

- Get personalized recommendations to move forward with your financing plans.

Also, discover business resources and tools to help you manage cash flow, build credit and grow with confidence.

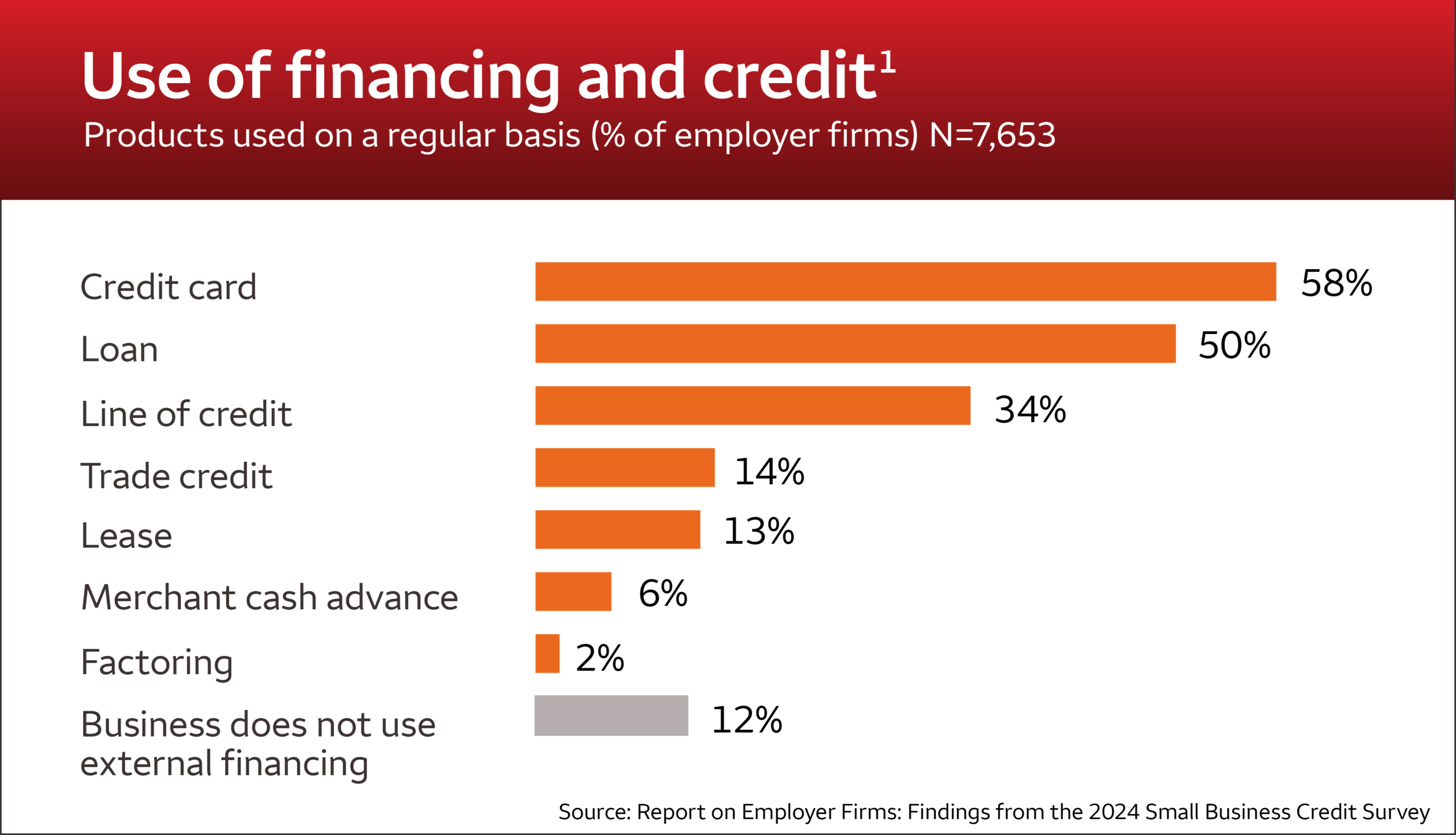

1 https://www.fedsmallbusiness.org/reports/survey/2025/2025-report-on-employer-firms

2 All financing is subject to credit approval and, if applicable, determination of SBA eligibility by Wells Fargo SBA Lending. Additional terms, conditions, and collateral may be required.

3 https://www.sba.gov/priorities/american-manufacturers/increasing-access-capital

4 This is not an exhaustive list of requirements for start-ups.

5 https://jbakerlawgroup.com/what-is-the-difference-between-seller-financing-vs-traditional-loans

6 https://federalreserve.gov/publications/2025-march-consumer-community-context.htm